Analyzing the Insurance Industry's First Open Source Policy From 2018: A Look at InsurTech Lemonade's "Policy 2.0"

Explore how Lemonade's 2018 Policy 2.0 merged insurance with the tech industry's open source principles, analyzing its impact on policy language, coverage structure, and insurtech marketing strategy. A deep dive into insurance innovation and tech-forward branding.

Explore how Lemonade's 2018 Policy 2.0 merged insurance with the tech industry's open source principles, analyzing its impact on policy language, coverage structure, and insurtech marketing strategy. A deep dive into insurance innovation and tech-forward branding.

The intersection of insurance and technology has produced numerous innovations in recent years, but few are as interesting from a historical perspective as the 2018 launch of an open source insurance policy (I'll cover what this means, and the insurtech significance of this, further in the article).

This initiative by insurtech company Lemonade marked an intriguing experiment in combining traditional insurance practices with tech industry concepts, while simultaneously serving as a sophisticated marketing strategy.

Understanding the Copyright and InsurTech Context of "Open Source"

Insurance policies have traditionally followed one of two paths: either using proprietary language developed by individual insurers, or building upon standardized ISO (Insurance Services Office) forms.

The ISO forms, which are copyrighted and licensed to insurers for a fee, have been the industry standard for decades. This system has created a relatively closed ecosystem where policy language is treated as proprietary intellectual property.

The concept of open source presents a stark contrast to this traditional approach. Open source, originally a software development practice, means making the source material freely available for anyone to view, modify, and use.

Think of it like a recipe that a restaurant makes public; not just letting people see the final dish, but sharing detailed instructions so others can make it, modify it, or use it as inspiration for their own creations. When something is open source, it's typically protected by special licenses that ensure it remains freely available even as it evolves. Examples of established open source licenses can include copyleft open source like Creative Commons, or (in this case) a GNU Free Documentation License.

Lemonade chose to license their policy under the GNU Free Documentation License (GFDL), a sister to the popular GNU General Public License used in software. This license, created by the Free Software Foundation, ensures that the policy and any derivatives must remain freely available.

It's similar to a "pay it forward" agreement - anyone can use and modify the policy, but they must share their modifications under the same terms. This is fundamentally different from traditional copyright, which restricts copying and modification, or ISO forms, which require payment and limit modification rights.

Since this license is related to software, that leads us into the link to insurtech.

The Tech Industry's Influence on Insurance

When insurtech company Lemonade announced Policy 2.0 in May 2018, they weren't just introducing a new insurance policy, they were deliberately applying Silicon Valley principles to traditional insurance practices.

As a public insurance adjuster, media agency owner, and coder, I personally believe their strategy was created to align with their market positioning as a tech-first insurance provider, differentiating them from traditional insurers. Differentiation and market positioning through brand persona are powerful marketing concepts. And, if there's one thing the insurance industry has shown they're adept at, it's effectively wielding the psychology behind branding and marketing.

Again, the concept of open source comes from the software industry, where code is made publicly available for anyone to view, modify, or use. By applying this concept to an insurance policy, Lemonade was effectively borrowing cultural cachet from the tech world. I believe this was a calculated move that reinforced their brand identity as an innovative insurtech company rather than a traditional insurer.

GitHub: The Platform (Most) of The Internet's Code is Served From

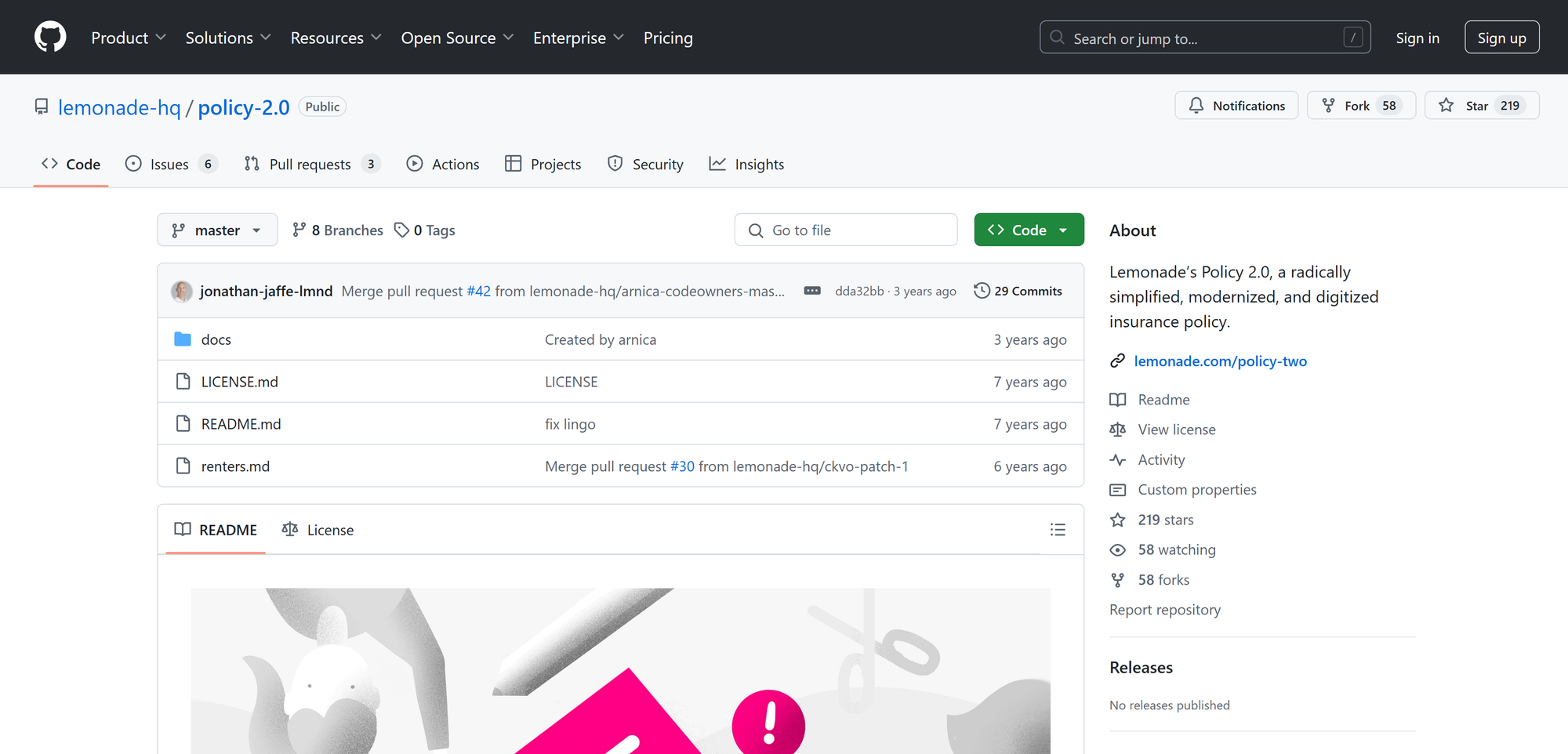

The decision to host Policy 2.0 on GitHub deserves particular analysis. GitHub serves as the primary platform where software developers store and share code. It's a massive digital library where most modern software's building blocks are stored and shared.

Attempting to simplify a confusing concept, think of GitHub like a magical coloring book where:

- Everyone can see everyone else's drawings (code)

- You can copy someone's drawing and make your own version

- You can suggest changes to other people's drawings

- The book remembers every change ever made, so you can always go back and see older versions

Most of the apps and websites you use every day—from social media platforms to banking apps—have their code stored on GitHub in some form. By choosing GitHub instead of traditional document sharing methods, I believe Lemonade was making a clear statement about their tech-first identity.

The Business Strategy Behind Open Source

The release of Policy 2.0 as open source came at a strategic time for Lemonade. As noted in their May 2018 press release, the company had recently secured $120 million in Series C funding and was planning global expansion. The open source announcement generated significant media attention and industry discussion, supporting their expansion narrative.

CEO Daniel Schreiber's statement about "dragging insurance into the 21st century" exemplifies the company's positioning strategy. By presenting traditional insurance as outdated, Lemonade was creating a narrative where their technological approach appeared as the logical next step in insurance evolution.

Great for Marketing, But is It Practical?

The technical aspects of Policy 2.0, its simplified language and digital-first approach, represent genuine innovations in policy design. However, the choice to make it open source appears to have served primarily as a branding exercise rather than a practical industry tool.

This observation isn't meant to diminish the initiative's significance; rather, it highlights how insurtech companies are effectively combining technical innovation with sophisticated marketing strategies.

Looking back from today, it's worth noting that while Policy 2.0 has been on GitHub for approximately 7 years, its practical impact on the industry has been more limited than its marketing impact.

The repository (a term used for where code is stored on GitHub) shows 8 branches and 219 stars (modest numbers in the open source world) and the last update was three years ago.

This suggests that while the initiative generated significant attention, it hasn't led to widespread industry adoption of open source insurance policies.

Policy Analysis and Coverage Implications

Even though the impact of this open source policy may have more affected positive marketing, rather than practical application, I still enjoyed analyzing the policy language.

Please keep in mind that since this is open source, and a base to work from, it likely was not meant to cover state-specific regulations or other factors. That's why it's open source, so the user can modify it for their needs. I encourage you to check out the policy for yourself in the citations section, and analyze for yourself! It's a great exercise for insurance professionals, to test your insurance industry experience and knowledge.

Getting into the policy, an examination of Policy 2.0's actual language and structure reveals both innovations and potential concerns:

Coverage Structure Innovations:

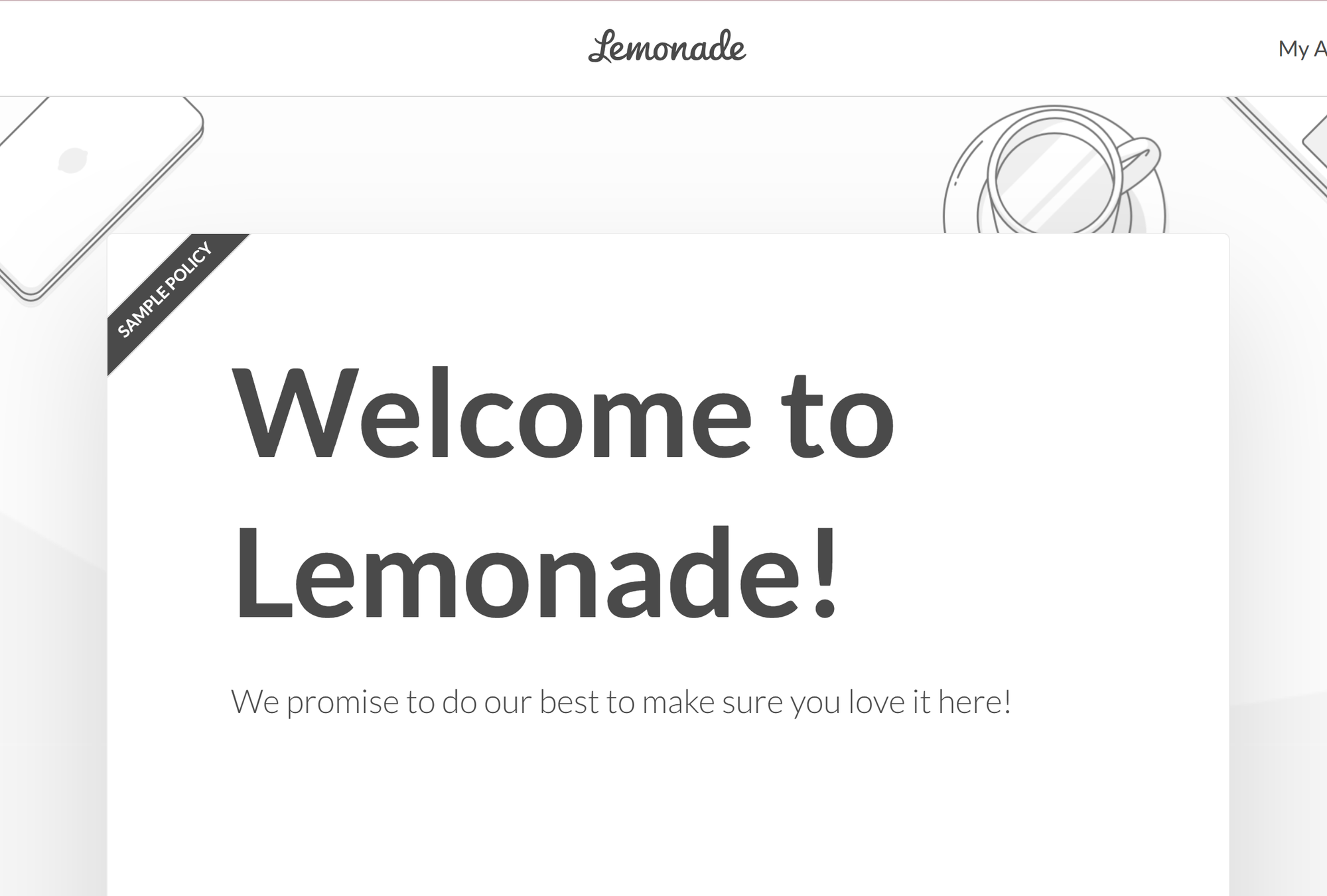

- Plain Language Approach—The policy replaces traditional insurance jargon with conversational explanations. For example, instead of defining "covered perils," it simply states "We protect you against theft, vandalism, fire, smoke, burst pipes, appliance leaks, and damage others may accuse you of causing."

- Clear Coverage Limits—The policy presents limits in a straightforward format, explicitly stating "$10,000 in total, and $2,500 per item" rather than burying these numbers in complex clauses.

- Modular Design—Additional coverages like "Bad Weather Package" and "Electronic Devices Package" are presented as optional add-ons, making customization more intuitive.

Coverage Concerns:

- Potential Coverage Gaps—The simplified language may create unintended coverage gaps. For instance, the policy's exclusion of "stuff that's used for your business" could create ambiguity in the work-from-home era.

- Broad Exclusions—The policy takes a notably broad approach to exclusions, stating that "Everything else, such as 'I lost it,' 'my dog ate it,' 'my kid dropped it'... aren't covered." This catchall approach might exclude what might be commonly covered losses in traditional policies.

- Limited Basic Coverage—The standard policy excludes several perils traditionally covered by competitors, such as weather-related damages, making them available only as add-on packages.

Notable Policy Elements:

- Deductible Explanation—The policy innovates by explaining deductibles through practical examples: "If you have an approved claim that amounts to $7,000, we will end up paying you $6,500."

- Claims Process—The policy emphasizes digital claims handling but maintains traditional requirements for proof of loss and cooperation.

- Valuation Method—The policy promises replacement cost coverage without depreciation, stating "We don't pay less just because your damaged item was used," which is clearer than traditional replacement cost provisions.

Legal and Regulatory Considerations:

- Arbitration Requirement—The policy maintains a mandatory arbitration clause despite its "simple" approach, potentially limiting policyholder rights. For context, most traditional property policies allow for filing suit, or for alternative dispute resolution methods like appraisal (not real estate appraisal, but the insurance-specific ADR method), and as more commonly utilized in a few states, mediation. Binding arbitration could be viewed as more extreme even to a lawsuit, as it can carry similar or more expensive costs, and is more restrictive in its practice and rules.

- State Variations—The policy acknowledges need for state-specific modifications with a placeholder section for state-required clarifications.

- Cancellation Terms—While simplified, the policy maintains legally required notice periods and premium refund provisions.

Discussion Points

Studying this policy and initiative, several questions emerged for me, which I hope you'll ponder on as well:

- How does the integration of tech industry practices into traditional insurance reflect broader industry trends?

- What does the limited practical adoption but significant marketing impact tell us about innovation in the insurance sector?

- How do regulatory requirements influence the potential for truly open source insurance products?

Closing Thoughts

In general, I really enjoyed stumbling upon and analyzing this open source policy, and the possible reasons behind this initiative.

It was quite interesting how I found it a couple of years ago. I first found and analyzed the German-language version of this, as I was helping a cousin in Germany find insurers! Funny how you find things.

Thank you for joining me into this deep-dive of insurtech history, and don't forget to share and subscribe so I can bring you more articles.

Citations

"Lemonade Launches World's First 'Open Source' Insurance Policy." BusinessWire, May 16, 2018. https://www.businesswire.com/news/home/20180516005661/en/

"Policy 2.0 Repository." GitHub, Lemonade, 2018-2025. https://github.com/lemonade-hq/policy-2.0

"The GNU Free Documentation License." Free Software Foundation, Version 1.3, 2008. https://www.gnu.org/licenses/fdl-1.3.html

"Lemonade Policy 2.0: World's First Open Source Insurance Policy." Lemonade, 2018. https://www.lemonade.com/policy-two

"Insurance Services Office." Wikipedia, 2024. https://en.wikipedia.org/wiki/Insurance_Services_Office