"The Task Grows Larger and More Hopeless": A 1907 View of Insurance Regulation That Reminds Us to Keep Going

Reading through a remarkable 1907 paper, I found both comfort and inspiration in realizing that our predecessors grappled with the same fundamental mission of balancing robust consumer protection with a healthy, competitive property insurance market.

It's easy to feel overwhelmed by the challenge of balancing robust consumer protection with a healthy, competitive property insurance market. Reading through a remarkable 1907 paper published by the American Economic Association, I found both comfort and inspiration in realizing that our predecessors grappled with the same fundamental mission.

The author, Maurice H. Robinson, writing in early 1907, captures this essential purpose beautifully. He argues that the state's role is to

"see that all forms of legitimate insurance are so conducted in principle and practice that they may minister to the largest possible number consistent with safety and economy."

This elegant articulation of regulatory purpose—ensuring both consumer access and market stability—could have been written today.

Sound Familiar?

Yet Robinson, writing in 1907, expresses familiar frustration with the pace of progress. He notes that even after "37 years of effort" (from the time of his writing in 1907, dating back to 1870), the National Association of (State) Insurance Commissioners was still striving toward uniform insurance regulation across states. As he rather pessimistically observes:

"The National Association of State Insurance Commissioners has been at work for thirty-seven years, and the task before it grows larger and more hopeless."

What's particularly striking is how Robinson understood the delicate balance regulators must strike. He emphasizes that insurance regulation should aim

"to secure an organization for each company so efficient and safe that insurance may be provided at the least possible cost and so representative in its government that every interest may receive its benefits in equitable proportion."

This dual focus on efficiency and fairness remains at the heart of modern insurance regulation.

Uniformity, Then and Now

The paper highlights how even then, there was significant push for standardization and coordination between states to achieve these goals. While perfect uniformity remains elusive, and may be something we'll always have to work toward, the progress since 1907 would likely amaze our predecessors. Today's NAIC has evolved into a robust organization that helps states coordinate their efforts to protect consumers while maintaining healthy insurance markets.

When we consider current challenges in insurance regulation—whether discussing principle-based reserving, group capital calculations, or international insurance standards—it's worth remembering that we're part of a much longer story of continuous improvement. The fact that we still grapple with some of the same fundamental challenges Robinson identified doesn't mean we haven't progressed; rather, it highlights the inherent complexity of balancing multiple stakeholder interests in insurance regulation.

Perhaps the most valuable lesson from this historical perspective is that progress, while sometimes frustratingly slow, does occur through sustained effort and collaboration. The regulatory framework we have today, despite its imperfections, represents significant progress in protecting both consumers and market stability - thanks to countless individuals who kept working despite feeling, at times, that the task was "hopeless."

So the next time you feel overwhelmed by the challenges of insurance regulation, remember Robinson and his colleagues from 1907. They couldn't see the progress their efforts would ultimately yield, but they kept going anyway, working toward that essential balance between consumer protection and market health. Of note, their efforts and hundreds of others, over decades, laid the groundwork for consumer protections as they exist today.

And that's exactly what we need to keep doing. How? Get involved with an association or nonprofit! Feel free to drop some suggestions in the comment below.

Citation

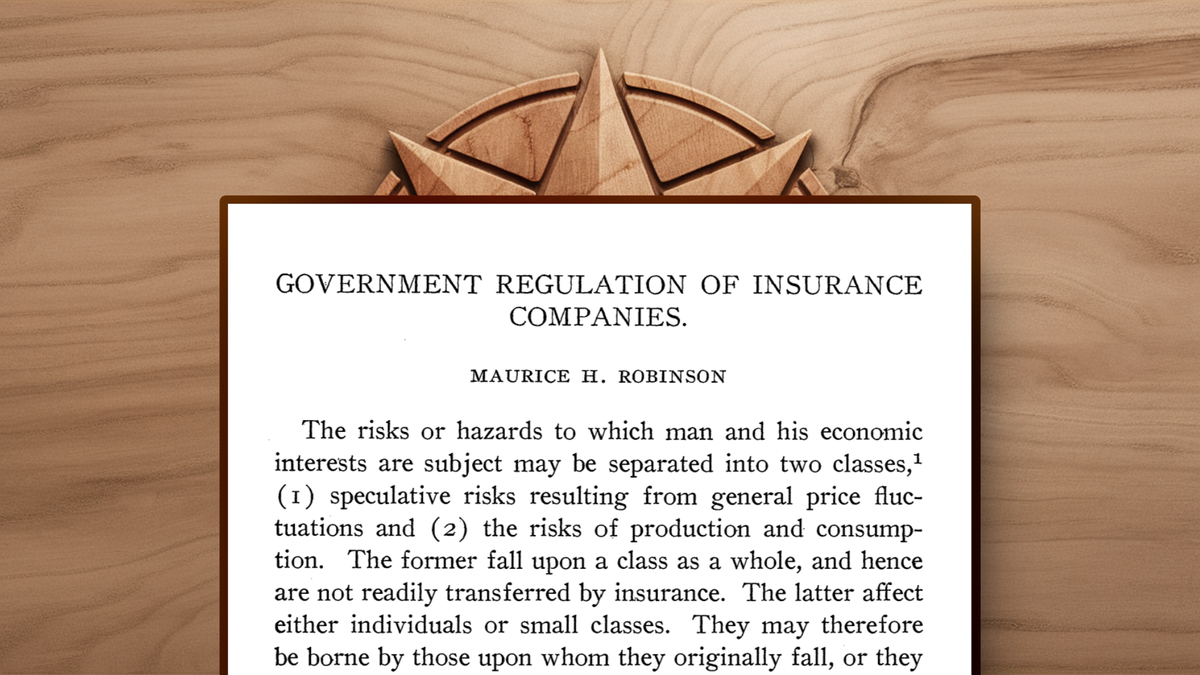

Robinson, Maurice H. “Government Regulation of Insurance Companies.” Publications of the American Economic Association, vol. 8, no. 1, 1907, pp. 137–54. JSTOR, http://www.jstor.org/stable/2999901. Accessed 16 Dec. 2024.